A 736 credit score is more than just a number; it's a gateway to numerous financial possibilities and advantages. As someone navigating the financial landscape, having a 736 credit score can open doors to better loan terms, lower interest rates, and increased bargaining power. Whether you're planning to apply for a mortgage, refinance an existing loan, or simply want to ensure you're on the right track financially, understanding the implications of your credit score is crucial.

In today's ever-evolving financial world, credit scores have become a critical component of one's financial health. Lenders, landlords, and even employers often use credit scores to assess your reliability and trustworthiness. A 736 credit score, which falls into the "good" range, can significantly influence your financial decisions and opportunities. This score reflects your ability to manage credit responsibly, and it can greatly impact your access to credit, loans, and even housing.

As you embark on this journey to understand what a 736 credit score entails, it's essential to delve into how it is calculated, its implications, and the strategies you can employ to maintain or improve it. This comprehensive guide will provide you with the insights you need to make informed financial decisions, ensuring that your credit score works in your favor to achieve your financial goals.

Table of Contents

- What is a Credit Score?

- Understanding the 736 Credit Score

- Factors Affecting Your Credit Score

- Benefits of a 736 Credit Score

- How to Maintain a Good Credit Score

- Common Misconceptions About Credit Scores

- Improving Your Credit Score

- The Role of Credit Reports

- Impact of Credit Scores on Loans and Mortgages

- Credit Score Myths Debunked

- Credit Score vs. Credit Report

- Protecting Your Credit Score

- Understanding Credit Score Impact on Employment

- Frequently Asked Questions

- Conclusion

What is a Credit Score?

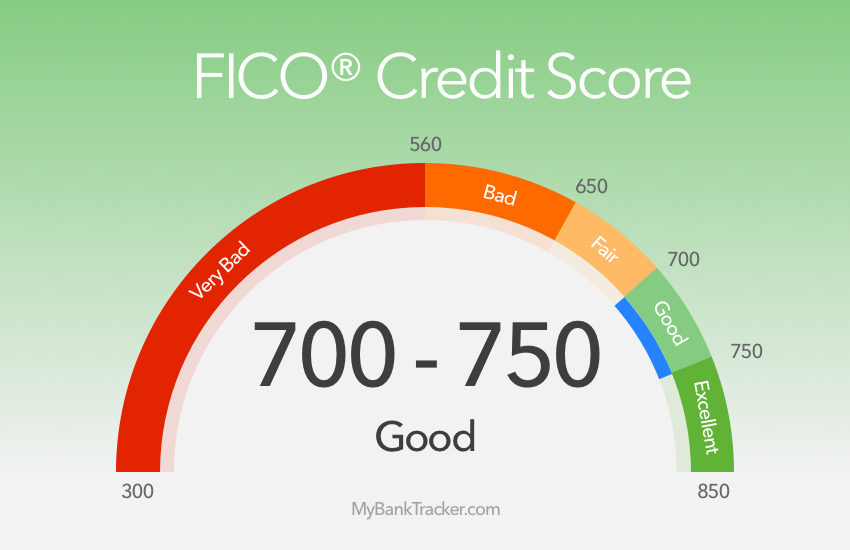

A credit score is a numerical representation of an individual's creditworthiness based on their credit history. This three-digit number is derived from credit reports, which contain detailed information about a person's credit activities, including the amount of debt they have, their repayment history, and the length of their credit history. Credit scores typically range from 300 to 850, with higher scores indicating better creditworthiness.

Credit scores are used by lenders to evaluate the risk of lending money to consumers. A higher credit score suggests that a borrower is more likely to repay their debts on time, making them a lower-risk candidate for loans and credit. Conversely, a lower credit score may indicate a higher risk, resulting in less favorable loan terms or even denial of credit.

The most commonly used credit scoring model is the FICO Score, developed by the Fair Isaac Corporation. Another widely used model is the VantageScore, which was created collaboratively by the three major credit bureaus: Experian, TransUnion, and Equifax. Both models utilize similar criteria to calculate credit scores, but they may weigh factors differently.

Understanding the 736 Credit Score

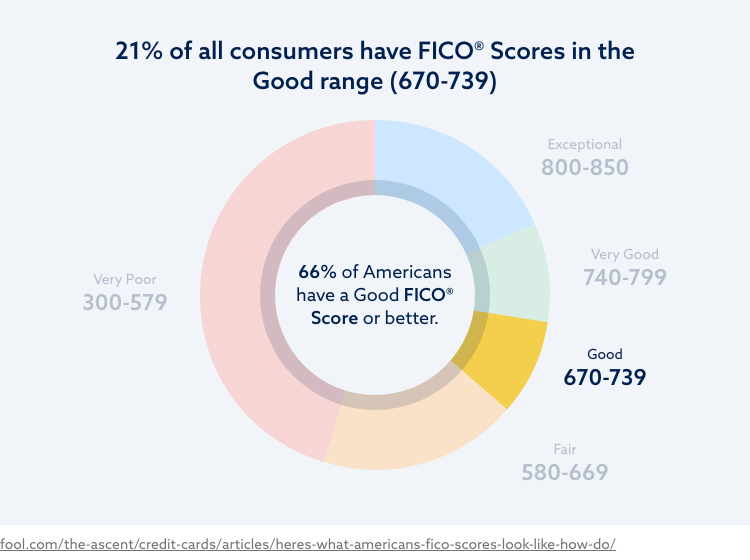

A 736 credit score falls within the "good" range on the FICO scale, which typically ranges from 670 to 739. This score suggests that you have a strong credit history and have managed your credit responsibly. Lenders view a 736 credit score as an indication that you pose a relatively low risk when it comes to borrowing money, which can lead to more favorable lending terms.

Having a credit score of 736 means that you are likely to qualify for a variety of credit products, such as credit cards, personal loans, and mortgages. You may also be eligible for competitive interest rates and favorable loan terms, which can save you money over time. Additionally, a 736 credit score can enhance your negotiating power when it comes to financial products.

Despite being in the "good" range, it's important to remember that credit scores can fluctuate based on your financial behavior. Maintaining or improving your score requires ongoing attention to your credit habits, including timely payments, responsible credit usage, and monitoring your credit reports for inaccuracies.

Factors Affecting Your Credit Score

Several key factors influence your credit score, and understanding these can help you maintain or improve your score over time. Here are the primary components that affect your credit score:

- Payment History: This is the most significant factor in calculating your credit score. It reflects your ability to make timely payments on credit accounts. Late payments, collections, and bankruptcies can have a negative impact on this aspect of your score.

- Credit Utilization: This factor measures the amount of credit you are using compared to your total available credit. A lower credit utilization rate is generally better for your score. It's recommended to keep this ratio below 30%.

- Credit History Length: The length of time you've been using credit also affects your score. A longer credit history demonstrates a track record of credit management, which can positively influence your score.

- Types of Credit Accounts: Having a mix of credit accounts, such as credit cards, installment loans, and retail accounts, can positively impact your score. It shows that you can manage different types of credit responsibly.

- Recent Credit Inquiries: Applying for new credit can result in hard inquiries on your credit report, which may temporarily lower your score. It's important to limit the number of hard inquiries to avoid negatively impacting your score.

Benefits of a 736 Credit Score

Having a 736 credit score comes with numerous advantages that can enhance your financial well-being. Here are some of the benefits you can enjoy with a credit score in this range:

- Competitive Loan Terms: With a 736 credit score, you're likely to qualify for loans with favorable terms, including lower interest rates and reduced fees. This can save you significant money over the life of a loan.

- Increased Credit Card Options: A good credit score can make you eligible for credit cards with attractive perks, such as cash back, travel rewards, and low introductory interest rates.

- Better Insurance Rates: Some insurance companies use credit scores to determine premiums. A higher credit score may result in lower insurance costs, particularly for auto and homeowners insurance.

- Greater Negotiating Power: When applying for credit, a good credit score gives you leverage to negotiate better terms and conditions, potentially leading to more favorable outcomes.

- Improved Housing Opportunities: Landlords often check credit scores as part of the rental application process. A 736 credit score can make you a more attractive tenant candidate, increasing your chances of securing a desirable rental property.

How to Maintain a Good Credit Score

Maintaining a good credit score requires consistent effort and responsible financial behavior. Here are some strategies to help you keep your credit score in the "good" range or even improve it over time:

- Pay Bills on Time: Timely payments are crucial for maintaining a good credit score. Set up reminders or automatic payments to ensure you never miss a due date.

- Monitor Credit Utilization: Keep your credit utilization ratio low by paying down credit card balances and avoiding maxing out credit limits.

- Regularly Review Credit Reports: Check your credit reports from all three major credit bureaus at least once a year. Dispute any inaccuracies that could negatively impact your score.

- Limit New Credit Applications: Be cautious about applying for new credit accounts, as multiple inquiries can lower your score. Only apply for credit when necessary.

- Maintain a Diverse Credit Mix: If possible, maintain a variety of credit types, such as installment loans and revolving credit, to demonstrate your ability to manage different forms of credit.

Common Misconceptions About Credit Scores

Despite the widespread use of credit scores, several misconceptions persist. Here are some common myths and the truths behind them:

- Checking Your Credit Lowers Your Score: Checking your own credit is considered a soft inquiry and does not affect your score. Regularly reviewing your credit can help you stay informed about your credit health.

- Closing Credit Cards Improves Your Score: Closing credit card accounts can actually hurt your score by reducing your overall credit limit and increasing your credit utilization ratio.

- Income Directly Affects Your Credit Score: While income can impact your ability to obtain credit, it is not directly factored into your credit score. Your score is based on your credit behavior, not your income level.

- All Debts Affect Your Credit Equally: Different types of debt are weighed differently. For example, revolving debt like credit cards can have a more significant impact on your score than installment debt such as student loans.

- Once a Negative Item is Removed, Your Score Will Skyrocket: Removing a negative item can help, but improvement takes time. Your score is influenced by multiple factors, so consistent positive behavior is key.

Improving Your Credit Score

If you're aiming to boost your credit score beyond 736, there are several proactive steps you can take. These strategies can help you enhance your credit profile and increase your score over time:

- Focus on Timely Payments: Ensure all your bills are paid on time, as late payments can significantly impact your score. Consider setting up automatic payments for fixed expenses.

- Reduce Credit Card Balances: Paying down existing credit card balances can lower your credit utilization ratio, positively impacting your score.

- Increase Credit Limits: If possible, request a credit limit increase on existing accounts. This can reduce your credit utilization and improve your score, provided you don't increase your spending.

- Consider a Secured Credit Card: If you're struggling to qualify for traditional credit, a secured credit card can help you build or rebuild your credit with responsible use.

- Keep Old Accounts Open: The length of your credit history matters, so keeping older accounts open can positively influence your score.

The Role of Credit Reports

Credit reports play a crucial role in determining your credit score. They provide a comprehensive overview of your credit history, detailing your credit accounts, payment history, and any negative information such as collections or bankruptcies. Credit reports are maintained by the three major credit bureaus: Experian, TransUnion, and Equifax.

Regularly reviewing your credit reports is essential for maintaining your credit health. By checking your reports, you can identify any discrepancies or errors that may negatively impact your score. If you find inaccuracies, it's important to dispute them with the relevant credit bureau to have them corrected.

In addition to affecting your credit score, credit reports are also used by lenders, landlords, and employers to assess your financial responsibility. Therefore, staying informed about your credit report can help you make informed decisions and take necessary actions to protect your creditworthiness.

Impact of Credit Scores on Loans and Mortgages

Your credit score has a significant impact on your ability to obtain loans and mortgages. Lenders use credit scores to assess the risk of lending to you, and a higher score can lead to more favorable loan terms. Here's how your credit score can influence your borrowing experience:

- Interest Rates: A higher credit score often results in lower interest rates on loans and mortgages. This means you'll pay less in interest over the life of the loan, potentially saving you thousands of dollars.

- Loan Approval: A good credit score increases your chances of being approved for loans and mortgages. Lenders are more likely to approve applications from individuals with a history of responsible credit management.

- Loan Amounts: With a higher credit score, you may qualify for larger loan amounts, allowing you to access the funds you need more easily.

- Down Payments: A good credit score can reduce the size of the down payment required for a mortgage, making homeownership more accessible.

Credit Score Myths Debunked

Credit scores are often misunderstood, leading to various myths and misconceptions. Let's debunk some common myths:

- All Credit Scores Are the Same: Different scoring models exist, and each may produce slightly different scores. It's important to understand which model a lender uses when evaluating your creditworthiness.

- Using a Credit Card Will Always Improve Your Score: While responsible credit card use can boost your score, maxing out cards or missing payments can have the opposite effect.

- Credit Repair Companies Can Instantly Boost Your Score: While some companies offer legitimate services, quick fixes are unlikely. Improving your score requires consistent, responsible credit behavior.

- Paying Off Debt Instantly Improves Your Score: Paying off debt can positively impact your score, but it may not lead to immediate changes. It takes time for credit bureaus to update your credit report.

Credit Score vs. Credit Report

While credit scores and credit reports are closely related, they serve distinct purposes in evaluating your creditworthiness:

- Credit Score: A credit score is a numerical representation of your creditworthiness, typically ranging from 300 to 850. It’s calculated based on information from your credit report, and it gives lenders a quick snapshot of your credit risk.

- Credit Report: A credit report is a detailed record of your credit history, including your credit accounts, payment history, and any negative information. It provides the data used to calculate your credit score.

Understanding the difference between the two can help you take better control of your credit health. Regularly reviewing both your credit score and credit report is essential for maintaining a good credit profile.

Protecting Your Credit Score

Safeguarding your credit score is essential for maintaining financial stability. Here are some proactive steps you can take to protect your credit score:

- Monitor Your Credit Regularly: Regularly check your credit reports and scores from the three major credit bureaus to stay informed about your credit health.

- Set Up Fraud Alerts: Consider setting up fraud alerts with the credit bureaus to be notified of any suspicious activity on your credit accounts.

- Use Credit Wisely: Avoid taking on unnecessary debt and use credit responsibly to maintain a healthy credit profile.

- Dispute Inaccuracies: If you find errors on your credit report, dispute them immediately to prevent them from negatively impacting your score.

Understanding Credit Score Impact on Employment

While credit scores are primarily used for lending decisions, they can also impact employment opportunities. Some employers check credit reports as part of the hiring process, particularly for positions that involve financial responsibilities. Here's how your credit score may affect your employment prospects:

- Background Checks: Employers may review your credit report to assess your financial responsibility and trustworthiness.

- Job Offers: A strong credit report can increase your chances of securing job offers, especially for roles that require handling financial transactions.

- Security Clearances: For positions that require security clearances, a good credit history can be a crucial factor in the approval process.

Frequently Asked Questions

What is a good credit score range?

A good credit score typically ranges from 670 to 739 on the FICO scale. A 736 credit score falls within this range, indicating a strong credit history.

Can a 736 credit score get me a mortgage?

Yes, with a 736 credit score, you're likely to qualify for a mortgage with favorable terms and competitive interest rates.

How can I improve my credit score quickly?

While there are no instant fixes, you can improve your score by making timely payments, reducing credit card balances, and avoiding new credit inquiries.

Does checking my credit report affect my score?

No, checking your own credit report is considered a soft inquiry and does not impact your credit score.

What factors negatively affect my credit score?

Late payments, high credit utilization, and multiple hard inquiries can negatively impact your credit score.

How often should I check my credit report?

You should check your credit report at least once a year from each of the three major credit bureaus to ensure accuracy and monitor for potential fraud.

Conclusion

Understanding your 736 credit score and its implications is an essential part of managing your financial health. With a score in the "good" range, you have access to favorable loan terms, increased credit opportunities, and the ability to negotiate better financial products. By staying informed about the factors that influence your score and taking proactive steps to maintain or improve it, you can ensure that your credit score continues to work in your favor.

Remember, a credit score is not static, and responsible financial behavior is key to maintaining a healthy credit profile. Whether you're planning to apply for a mortgage, refinance a loan, or simply want to improve your financial standing, understanding your credit score is the first step toward achieving your financial goals.

For more information on credit scores and financial management, consider visiting reputable financial websites or consulting with a financial advisor to gain further insights into how you can make the most of your credit score.

Exploring The World Of Www Downloadhub Vc: A Comprehensive Guide

Exploring The Life And Legacy Of Marni Turner: A Journey Of Inspiration And Achievement

Unveiling The World Of Downloadhub.tours: A Comprehensive Guide